Let’s settle this first: That ₹2 crore term insurance plan isn’t just about life coverage — it’s one of the smartest tax-planning tools in your arsenal. But most taxpayers only scratch the surface.

Why ₹2 Crore Term Insurance Coverage is the New Baseline?

Before we dive into tax benefits, understand why ₹2 crore term insurance matters:

● Education Inflation: A child’s MBA costing ₹20 lakh today could cost over ₹43 lakh in 10 years (assuming 8% annual inflation)*

● Home Loans: Average metro city home loans now approach or exceed ₹1 crore

● Income Replacement: Maintains lifestyle for dependents (30X annual income rule)

*Indicative figure; actual inflation may vary. Source: Private financial planning reports.

The Tax Advantage:

Unlike investments, term insurance combines protection with tax savings under:

● Section 80C (Premiums paid)

● Section 10(10D) (Death benefit received)

● Section 80D (Eligible riders like critical illness)

How to Extract Every Rupee of Benefit Legally?

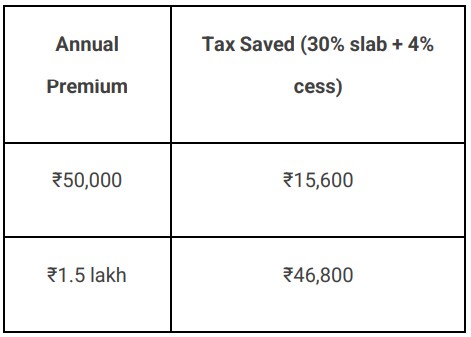

- Section 80C: Cut Your Tax Like a Pro

(Strategic premium planning for salaried & self-employed individuals)

How Much Can You Save?

Assumes full deduction available under Section 80C. Individual savings may vary.

The 10% Rule Demystified

For your ₹2 crore term insurance policy:

● To qualify for tax-free proceeds under Section 10(10D), the annual premium must not exceed 10% of the sum assured

● Example: ₹20 lakh/year is 10% of ₹2 crore

Reality Check:

Most term plans cost just 0.1%–0.3% of the sum assured (₹20,000–₹60,000/year)

Pro Tip:

Combine with other 80C instruments for the full ₹1.5 lakh deduction:

● ₹50K term insurance premium

● ₹70K ELSS

● ₹30K PPF

2. Section 10(10D): Ensuring Tax-Free Claims

(Where some nominees may miss benefits unintentionally)

Claim Settlement Checklist

● Nominee Awareness:

Educate nominees that term insurance payouts are tax-free under Section

10(10D) (subject to conditions)

● Document Safeguarding:

○ Policy bond (physical + digital copy)

○ Last 3 years’ premium receipts

○ Death certificate (with English translation if required)

● Timely Intimation:

Most insurers require notification within 90 days of death

Critical Exception (for ROP Plans)

● Death or maturity benefits may become taxable if:

○ Premiums exceed 10% of the sum assured

○ Policy is surrendered before maturity

3. Hidden Tax Benefits Most Miss

a) Health Riders (Section 80D)

● Critical illness rider: Additional ₹25,000 deduction

● Senior citizen parent coverage: ₹50,000 deduction

b) Premium Frequency & GST Implication

● GST is charged at 18%, but annual premium payments may cost less due to insurer-offered discounts

● Example: Annual premium may result in slightly lower GST compared to monthly payments

GST amount does not change with frequency; savings result from discounts.

c) NRI-Specific Advantages

● Premiums paid remain eligible under Section 80C, if income is taxable in India

● Claims are repatriable under the Liberalised Remittance Scheme (LRS) — Subject to a $250,000/year limit

4. Costly Mistakes to Avoid

● Mistake 1: Not updating nominees after life events

Case Study: A Mumbai executive’s ₹2 crore term insurance went to his ex-wife as

he didn’t update the nominee post-divorce

● Mistake 2: Choosing the cheapest premium blindly

○ Slower claim settlements

○ Stricter underwriting

○ Rider-related exclusions

● Mistake 3: Assuming portability applies

○ Unlike health insurance, term plans are not portable — a new plan involves

new underwriting

○ Previous 80C benefits do not carry forward with a switch

5. Your Action Plan

For Salaried Individuals

● Adjust Form 16 declarations to reflect premiums paid

● Claim HRA separately — term insurance premiums do not affect HRA calculations

For Business Owners

● Only keyman insurance premiums are eligible as business expenses

● These payouts may be taxable

● Maintain separate records for insurance-related GST credits, if applicable

Final Calculation: ₹2 Crore Term Insurance Value

For a 35-year-old in the 30% tax bracket:

● Annual Tax Saved: Up to ₹46,800

● Lifetime Protection: ₹2 crore, tax-free

● Net Cost After Tax Savings: As low as ₹1,100/month (based on illustrative premiums)

The Bottom Line:

This isn’t just term insurance — it’s tax-efficient wealth protection that keeps your hardearned money where it belongs: with your family.

👉 Click here to read the latest Gujarat news on TheLiveAhmedabad.com